Skatteudvalget 2012-13

L 10 Bilag 12

Offentligt

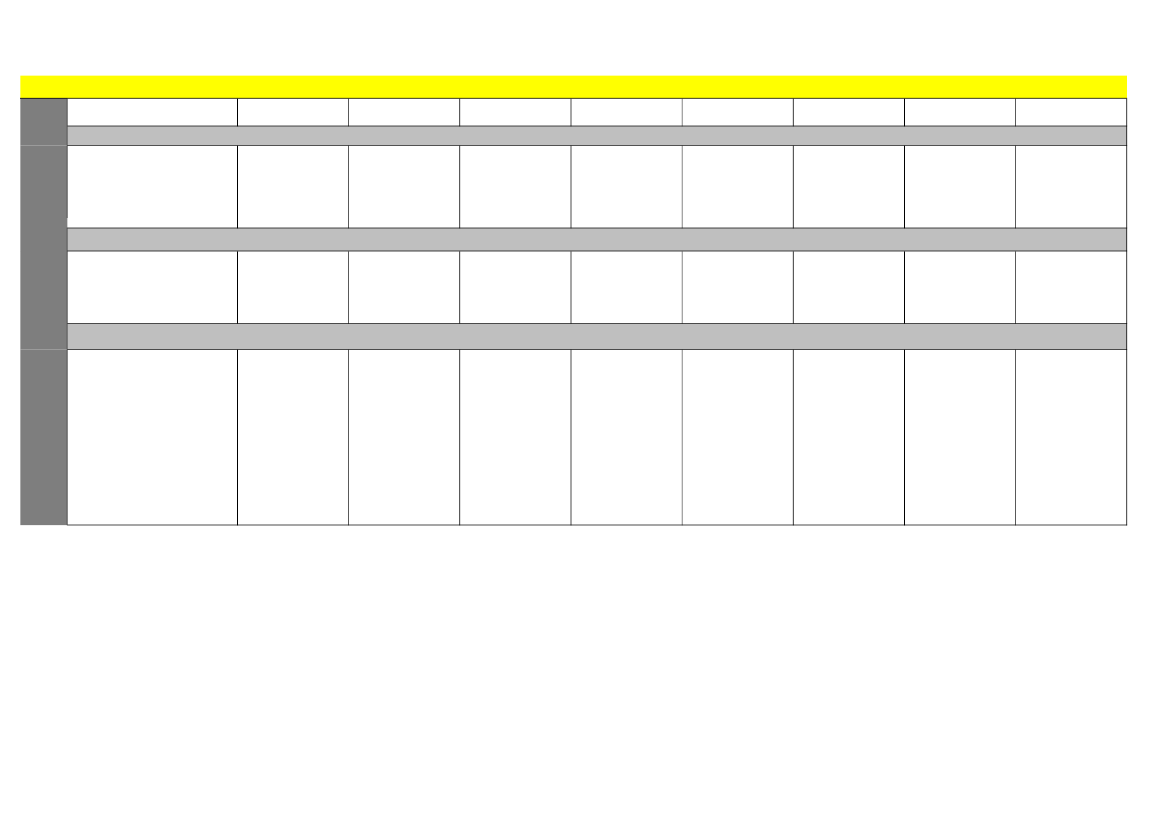

High-level overview of taxation of investorsLocal resident Corporate investor - less Local resident Corporate investor – atthan 10% ownershipleast 10% ownershipEU/EEC resident Corporate investor -less than 10% ownershipEU/EEC resident Corporate investor –at least 10% ownershipTreaty resident Corporate investor -less than 10% ownershipTreaty resident Corporate investor – atleast 10% ownershipNon EU/EEC/Treaty residentCorporate investor - less than 10%ownershipNon EU/EEC/Treaty residentCorporate investor – at least 10%ownership

1. Sale of shares in Holdco to a third party

Treatment/classification of sales priceBasis of taxationLevel of taxation

Capital gainGain only25%

Capital gainGain onlyParticipation exemption

N/AN/ANot subject to DK tax

N/AN/ANot subject to DK tax

N/AN/ANot subject to DK tax

N/AN/ANot subject to DK tax

N/AN/ANot subject to DK tax

N/AN/ANot subject to DK tax

2. Dividend distribution from Holdco, fundedby dividends received from OpcoTreatment/classification of distributionDividendEntire amount25%DividendEntire amountParticipation exemptionDividendEntire amount15%DividendEntire amountParticipation exemptionDividendEntire amount15%DividendEntire amount27% but reduced undertreaty and thus eliminatedDividendEntire amount15% or 27%DividendEntire amount27%

DENMARK

Basis of taxationLevel of taxation3. Exit of investment (sale of Opco to thirdparty, repatriation of funds to investors)Most beneficial tax treatment

zero taxation in Denmark

zero taxation in Denmark

zero taxation in Denmark

zero taxation in Denmark

zero taxation in Denmark

zero taxation in Denmark

zero taxation in Denmark

zero taxation in Denmark

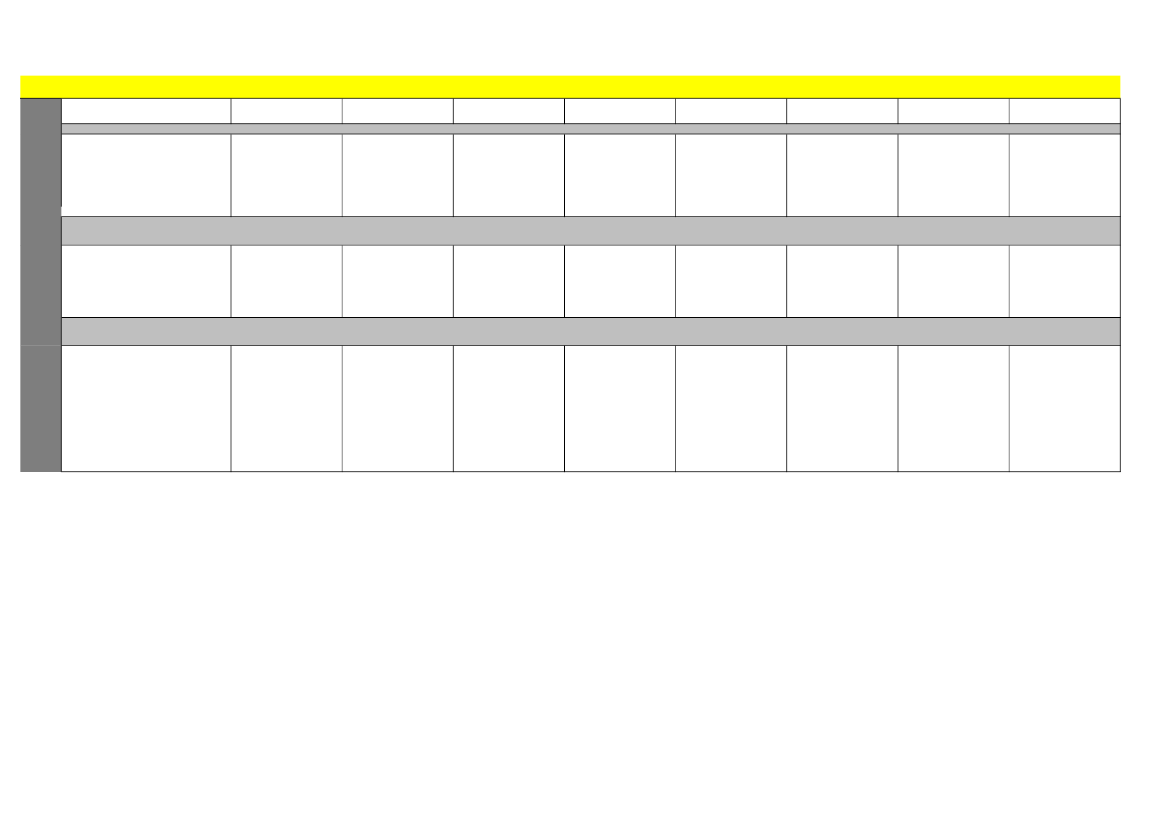

Action (very brief description)After L10 in current form

Sale of Holdco to local sistercompany (Newco) againstdebt. Holdco distributesdividends to Newco andNewco repays debt.Dividend payment

Sale of Holdco to local sistercompany (Newco) againstdebt. Holdco distributesdividends to Newco andNewco repays debt.Dividend payment

Sale of Holdco to local sistercompany (Newco) againstdebt. Holdco distributesdividends to Newco andNewco repays debt.Dividend payment

Sale of Holdco to local sistercompany (Newco) againstdebt. Holdco distributesdividends to Newco andNewco repays debt.

Sale of Holdco to local sistercompany (Newco) againstdebt. Holdco distributesdividends to Newco andNewco repays debt.

Most beneficial tax treatment

Dividends taxation, entireamountPrevious method no longeravailable.

Participation exemption

Dividends taxation, entireamountPrevious method no longeravailable.

Participation exemption

Dividends taxation, entireamountPrevious method no longeravailable.

Participation exemption

Dividends taxation, entireamountPrevious method no longeravailable.

Dividends taxation, entireamountPrevious method no longeravailable.

Action (very brief description)

Previous method OK.

Previous method OK.

Previous method OK.

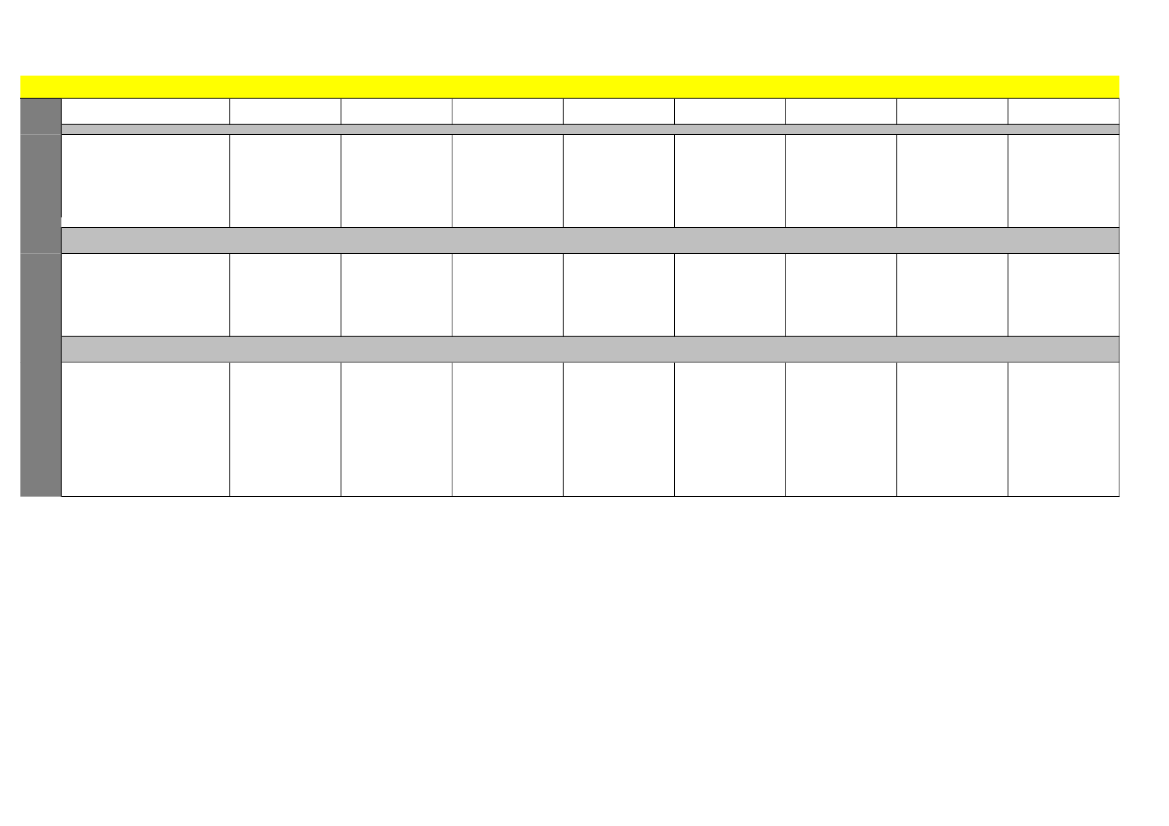

High-level overview of taxation of investorsLocal resident Corporate investor - less Local resident Corporate investor – atthan 10% ownershipleast 10% ownershipEU/EEC resident Corporate investor -less than 10% ownershipEU/EEC resident Corporate investor –at least 10% ownershipTreaty resident Corporate investor -less than 10% ownershipTreaty resident Corporate investor – atleast 10% ownershipNon EU/EEC/Treaty residentCorporate investor - less than 10%ownershipNon EU/EEC/Treaty residentCorporate investor – at least 10%ownership

1. Sale of shares in Holdco to a third partyTreatment/classification of sales priceBasis of taxationLevel of taxationCapital gainGain onlyParticipation exemption*Capital gainGain onlyParticipation exemption*N/AN/ANot subject to Swe taxN/AN/ANot subject to Swe taxN/AN/ANot subject to Swe taxN/AN/ANot subject to Swe taxN/AN/ANot subject to Swe taxN/AN/ANot subject to Swe tax

2. Dividend distribution from Holdco, fundedby dividends received from Opco

SWEDEN

Treatment/classification of distributionBasis of taxationLevel of taxation3. Exit of investment (sale of Opco to thirdparty, repatriation of funds to investors)Most beneficial tax treatmentAction (very brief description)

DividendEntire amountParticipation exemption*

DividendEntire amountParticipation exemption*

DividendEntire amountWHT 0-15%****

DividendEntire amountWHT 0%***

DividendEntire amountWHT 0-25%****

DividendEntire amountWHT 0-25%****

DividendEntire amountWHT 0%** or 30%

DividendEntire amountWHT 0%** or 30%

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestoralso subject to participationexemption + no wht

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestoralso subject to participationexemption + no wht

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestor0-15% whtSee ** (if company no SweWHT)

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestor0-15% whtSee ** (if company no SweWHT)

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestor0-25% whtSee ** (if company no SweWHT)

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestor0-25% whtSee ** (if company no SweWHT)

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestor0% or 30%See ** (if tax haven - 30%WHT))

Participation exemption*Sale of OpCo By HoldConot trigger tax - participationexemption, dividend toinvestor0% or 30%

See ** (if tax haven 30%)

* Under the Swedish participation exemption regime Swedish limited companies (ktiebolag, or ABs) are exempt from tax oncapital gainsderived from disposals of business-related shares. Thisaexemption also applies to European Union (EU) companies with a permanent establishment in Sweden if the shares are allocated to the permanent establishment. All unlisted shares are consideredbusiness-related and, consequently, qualify for the exemption. Listed shares are considered to be business-related if the company holds at least 10% of the voting rights or if the shares are held fororganizational purposes in the course of the business. No minimum holding period will be required to qualify for the tax exemption on sales of unlisted shares, but a one-year holding period requirementwill apply to sales of listed shares. The participation exemption also implies thatdividendson business-related shares are exempt from tax in the recipient company.**Dividends paid to a foreign company (other than a tax haven company) that is equivalent to a Swedish company are based on Swedish law exempt from wht if the shares are held for business purposes*** No wht if the receiving EU legal entity meets the requirements laid down in Article 2 of the EU directive 2011/96/EU**** Depending on tax treaty requirements are met, standard wht based on Swedish law is 30%

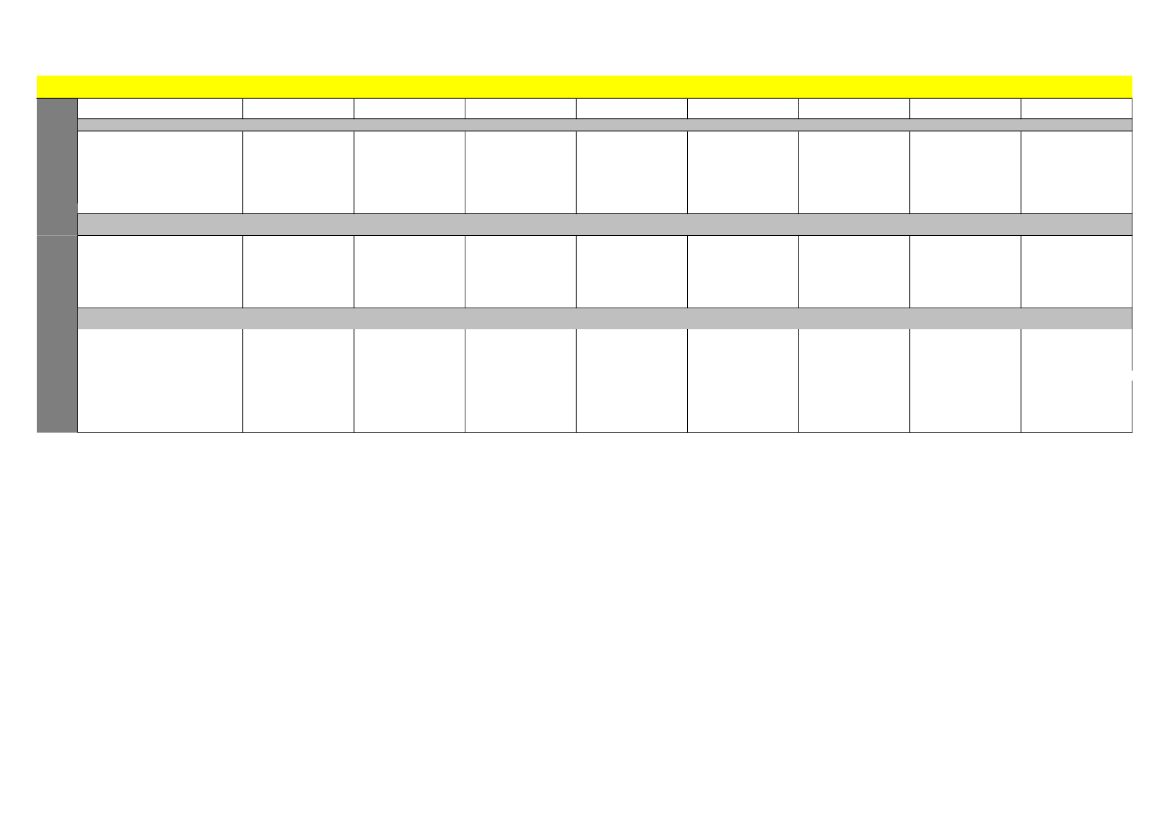

High-level overview of taxation of investorsLocal resident Corporate investor - less Local resident Corporate investor – atthan 10% ownershipleast 10% ownershipEU/EEC resident Corporate investor -less than 10% ownershipEU/EEC resident Corporate investor –at least 10% ownershipTreaty resident Corporate investor -less than 10% ownershipTreaty resident Corporate investor – atleast 10% ownershipNon EU/EEC/Treaty residentCorporate investor - less than 10%ownershipNon EU/EEC/Treaty residentCorporate investor – at least 10%ownership

1. Sale of shares in Holdco to a third partyTreatment/classification of sales priceBasis of taxationCapital gainGainCapital gainGainN/AN/AN/AN/AN/AN/AN/AN/AN/AN/AN/AN/A

Level of taxation

Tax free

Tax free

Not subject to tax in Norway

Not subject to tax in Norway

Not subject to tax in Norway

Not subject to tax in Norway

Not subject to tax in Norway

Not subject to tax in Norway

2. Dividend distribution from Holdco, fundedby dividends received from Opco

NORWAY

Treatment/classification of distributionBasis of taxation

DividendEntire amount

DividendEntire amount97% tax exempt (no tax ifwithin tax group)

DividendEntire amount

DividendEntire amount

DividendEntire amount

DividendEntire amount0-15% depending onownership

DividendEntire amount

DividendEntire amount

Level of taxation3. Exit of investment (sale of Opco to thirdparty, repatriation of funds to investors)Most beneficial tax treatment

97% tax exempt

Tax exempt

Tax exempt

In general 15%

25%

25%

Zero taxation in Norway

Zero taxation in Norway

Zero taxation in Norway

Zero taxation in Norway

Zero taxation in Norway

Zero taxation in Norway

Zero taxation in Norway

Zero taxation in Norway

Action (very brief description)

tax free liquidation of Holdco tax free liquidation of Holdco tax free liquidation of Holdco tax free liquidation of Holdco tax free liquidation of Holdco tax free liquidation of Holdco tax free liquidation of Holdco tax free liquidation of Holdco(treated as capital gains from (treated as capital gains from (treated as capital gains from (treated as capital gains from (treated as capital gains from (treated as capital gains from (treated as capital gains from (treated as capital gains froma Norwegian perspective)a Norwegian perspective)a Norwegian perspective)a Norwegian perspective)a Norwegian perspective)a Norwegian perspective)a Norwegian perspective)a Norwegian perspective)

High-level overview of taxation of investorsLocal resident Corporate investor - less Local resident Corporate investor – atthan 10% ownershipleast 10% ownershipEU/EEC resident Corporate investor -less than 10% ownershipEU/EEC resident Corporate investor –at least 10% ownershipTreaty resident Corporate investor -less than 10% ownershipTreaty resident Corporate investor – atleast 10% ownershipNon EU/EEC/Treaty residentCorporate investor - less than 10%ownershipNon EU/EEC/Treaty residentCorporate investor – at least 10%ownership

1. Sale of shares in Holdco to a third partyTreatment/classification of sales priceBasis of taxationLevel of taxationCapital gainGain only24% (Note 1)Capital gainGain onlyCapital gainGain onlyCapital gainGain onlyNot subject to UK taxCapital gainGain onlyNot subject to UK taxCapital gainGain onlyNot subject to UK taxCapital gainGain onlyNot subject to UK taxCapital gainGain onlyNot subject to UK tax

0% - Substantial shareholding Not subject to UK taxexemption

UNITED KINGDOM

2. Dividend distribution from Holdco, fundedby dividends received from OpcoTreatment/classification of distributionBasis of taxationLevel of taxation3. Exit of investment (sale of Opco to thirdparty, repatriation of funds to investors)Most beneficial tax treatmentAction (very brief description)Zero taxation in the UKSale of Opco followed bydividend payment by HoldcoZero taxation in the UKZero taxation in the UKZero taxation in the UKZero taxation in the UKZero taxation in the UKZero taxation in the UKZero taxation in the UKDividendEntire amountExemptDividendEntire amountExemptDividendEntire amountNo UK withholding taxDividendEntire amountNo UK withholding taxDividendEntire amountNo UK withholding taxDividendEntire amountNo UK withholding taxDividendEntire amountNo UK withholding taxDividendEntire amountNo UK withholding tax

Either sale of Holdco, or sale Either sale of Holdco, or sale Either sale of Holdco, or sale Either sale of Holdco, or sale Either sale of Holdco, or sale Either sale of Holdco, or sale Either sale of Holdco, or saleof Opco followed by a dividendof Opco followed by a dividendof Opco followed by a dividendof Opco followed by a dividendof Opco followed by a dividendof Opco followed by a dividendof Opco followed by a dividendpayment by Holdcopayment by Holdcopayment by Holdcopayment by Holdcopayment by Holdcopayment by Holdcopayment by Holdco

Note 1 - 24% in finanicial year 2012/13, 23% in finanicial year 2013/14